Presentation On Consumer Finance 3y6c2w

This document was ed by and they confirmed that they have the permission to share it. If you are author or own the copyright of this book, please report to us by using this report form. Report 3i3n4

Overview 26281t

& View Presentation On Consumer Finance as PDF for free.

More details 6y5l6z

- Words: 842

- Pages: 27

Presentation on Consumer Finance in India

Presented by Javed Hussain Kirti Jindal Karishma Bhandari Garima Dubey Garima Swami Hitesh Rajpurohit Gaurav yadav Hitesh Jeengar

Contents • • • • • • • •

Defination Durables which are financed Growth of consumer durables Future prospects of consumer finance Consumer finance growth drivers Consumer finance in Rural market About Bajaj Finance Organizational Hierarchy of Bajaj Finance

(Contd..) • • • • • • • •

Document required for financing Interest rates of finance Basis of Segmenting market Legal Procedure Situation of cases Limit of Finance Process of financing in Bajaj Finance Conclusion

Defination Consumer finance in the most basic sense of the word refers to any kind of lending to consumers. One of the best ways to get the unsecured loans is through the consumer finance.

Durables which are financed • • • • • • •

Television Washing Machine Air Conditioner DVD/VCD players Refrigerator Computers/laptops And other consumer durables

Growth of Consumer Durables • Cyclical & Seasonal Demand • Demand in Rural India • Consumer Awareness & Preference for new models • Attractive consumers loan schemes • Growth of Media • Use of Internet by Market Functionaries

Future prospects of Consumer Finance • Growth of GDP • Opportunities in Rural Market • Schemes of Banks & Financial Institutions • Increasing Consumer Awareness

FICCI Research •

Report-

1. 2. 3. 4. 5.

Attractive Schemes Phenomenal growth of Media Use of Internet The ability of Imports Reduction in Import duties and Input costs

•

Table of Projected growth in Prodction

Projected growth in production of Consumer Durables(Table) • • • • • • • • • • •

Refrigerator Air conditioner Washing Machines Microwave Ovens Consumer Electronics(overall) Colour televisions Black & White televisions VCDs/MP3 DVD Clock Watch -

5-10% 20-25% 5-10% - 25% 9% 15-20% 20% 30% 25% 10% 10%

(Source-FICCI report 05-06)

RURAL MARKET AND CONSUMER FINANCE

• Sales were high during festive season. • Rural people feel ease in giving installments instead of single down payment. • Rural persons found consumer loans useful because consumer durables are used for productive purposes.

PROBLEMS FACED IN RURAL SECTORS • Process of sanctioning loans,documentation and formalities takes too much time. • Higher interest rates for quicker sanctioning of loans. • People want advance information about the documents needed for taking loan.

RECOVERY OF LOANS • Recovery of loans is the toughest job in rural area. • Recovery rates are higher in cooperative banks. • Schemes for hardcore defaulters discourages the consumers who pay on time.

About Bajaj Capital BFL was created by the three-way demerger of Bajaj Auto, inheriting the insurance and finance businesses. Now, it is into consumer finance through listed firm Bajaj Auto Finance. It is also into general and life insurance businesses in JVs with Allianz. Bajaj Auto Finance, which initially financed purchases from Bajaj Auto, is now changing into a consumer finance firm. Last year, auto finance brought 55% business while 45% came from personal loans and financing consumer durables and PCs.

Organization Hierarchy • • • • •

There are four Departments: Sales Operational Credit Collection

Hierarchy of Sales Department Sales Dep

HOD

2-3 Member

3-5 TL

6-8 Exec.

Documents Required • ID • Income Proof • Address Proof Interest Rate For Dealer 0% rate For consumers on Durables 5%-8% rate Maximum 11%

Segmentation of Market Step 1 – Segmenting Market on Basis of Cities Step 2 – Grading Cities - A Grade - B Grade - C Grade - D Grade Step 3 – Deg Schemes Acc. to to Grades given

Legal Procedure Reserve Bank of India has told banks that the recovery agents appointed by them cannot re-possess by resorting to illegal means, vehicles or property or any other goods, in case of defaults by borrowers.

Situation of Cases Previously Till Oct 07 – 700 to 800 cases per Month

Action Taken Income proof made Essential Now 152 Cases Per month

Limit of Finance • Minimum Limit is of Rs.7000 • Maximum Limit is of Rs.500000 Base for deciding limit - Self Employed - 60000 in ITR - Salaried person – 5000 per mth

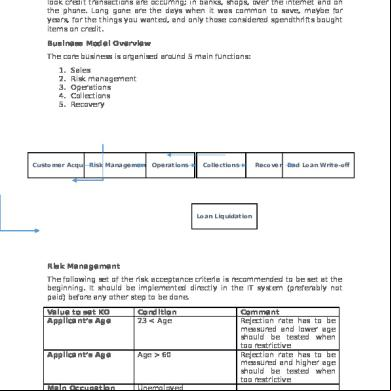

Process of consumer Finance • Consumer meet with dealer - Purchase decision - Filling of form - Submitting documents • Transfer of document from dealer to finance company • Checking of details by Operation Department • Transfer from Operation to Finance Department • Finance given to customer • Finally Collection Department collects the installments paid by customer (In case of default on finance collection department take legal action against customer)

Conclusion There are many organizations in the world which are providing consumer credit services which are helpful for the financial stability. Financial stability is very important not only for the businesses but also for the consumers. The businesses and as well as the consumers need the stability regarding the financial matters because without the stability no one could be very innovative in the longer run.

Special thanks to • Bajaj Finance – Manish Parekh

Sources of Information - Bajaj Finance - FICCI Report - Internet

Presented by Javed Hussain Kirti Jindal Karishma Bhandari Garima Dubey Garima Swami Hitesh Rajpurohit Gaurav yadav Hitesh Jeengar

Contents • • • • • • • •

Defination Durables which are financed Growth of consumer durables Future prospects of consumer finance Consumer finance growth drivers Consumer finance in Rural market About Bajaj Finance Organizational Hierarchy of Bajaj Finance

(Contd..) • • • • • • • •

Document required for financing Interest rates of finance Basis of Segmenting market Legal Procedure Situation of cases Limit of Finance Process of financing in Bajaj Finance Conclusion

Defination Consumer finance in the most basic sense of the word refers to any kind of lending to consumers. One of the best ways to get the unsecured loans is through the consumer finance.

Durables which are financed • • • • • • •

Television Washing Machine Air Conditioner DVD/VCD players Refrigerator Computers/laptops And other consumer durables

Growth of Consumer Durables • Cyclical & Seasonal Demand • Demand in Rural India • Consumer Awareness & Preference for new models • Attractive consumers loan schemes • Growth of Media • Use of Internet by Market Functionaries

Future prospects of Consumer Finance • Growth of GDP • Opportunities in Rural Market • Schemes of Banks & Financial Institutions • Increasing Consumer Awareness

FICCI Research •

Report-

1. 2. 3. 4. 5.

Attractive Schemes Phenomenal growth of Media Use of Internet The ability of Imports Reduction in Import duties and Input costs

•

Table of Projected growth in Prodction

Projected growth in production of Consumer Durables(Table) • • • • • • • • • • •

Refrigerator Air conditioner Washing Machines Microwave Ovens Consumer Electronics(overall) Colour televisions Black & White televisions VCDs/MP3 DVD Clock Watch -

5-10% 20-25% 5-10% - 25% 9% 15-20% 20% 30% 25% 10% 10%

(Source-FICCI report 05-06)

RURAL MARKET AND CONSUMER FINANCE

• Sales were high during festive season. • Rural people feel ease in giving installments instead of single down payment. • Rural persons found consumer loans useful because consumer durables are used for productive purposes.

PROBLEMS FACED IN RURAL SECTORS • Process of sanctioning loans,documentation and formalities takes too much time. • Higher interest rates for quicker sanctioning of loans. • People want advance information about the documents needed for taking loan.

RECOVERY OF LOANS • Recovery of loans is the toughest job in rural area. • Recovery rates are higher in cooperative banks. • Schemes for hardcore defaulters discourages the consumers who pay on time.

About Bajaj Capital BFL was created by the three-way demerger of Bajaj Auto, inheriting the insurance and finance businesses. Now, it is into consumer finance through listed firm Bajaj Auto Finance. It is also into general and life insurance businesses in JVs with Allianz. Bajaj Auto Finance, which initially financed purchases from Bajaj Auto, is now changing into a consumer finance firm. Last year, auto finance brought 55% business while 45% came from personal loans and financing consumer durables and PCs.

Organization Hierarchy • • • • •

There are four Departments: Sales Operational Credit Collection

Hierarchy of Sales Department Sales Dep

HOD

2-3 Member

3-5 TL

6-8 Exec.

Documents Required • ID • Income Proof • Address Proof Interest Rate For Dealer 0% rate For consumers on Durables 5%-8% rate Maximum 11%

Segmentation of Market Step 1 – Segmenting Market on Basis of Cities Step 2 – Grading Cities - A Grade - B Grade - C Grade - D Grade Step 3 – Deg Schemes Acc. to to Grades given

Legal Procedure Reserve Bank of India has told banks that the recovery agents appointed by them cannot re-possess by resorting to illegal means, vehicles or property or any other goods, in case of defaults by borrowers.

Situation of Cases Previously Till Oct 07 – 700 to 800 cases per Month

Action Taken Income proof made Essential Now 152 Cases Per month

Limit of Finance • Minimum Limit is of Rs.7000 • Maximum Limit is of Rs.500000 Base for deciding limit - Self Employed - 60000 in ITR - Salaried person – 5000 per mth

Process of consumer Finance • Consumer meet with dealer - Purchase decision - Filling of form - Submitting documents • Transfer of document from dealer to finance company • Checking of details by Operation Department • Transfer from Operation to Finance Department • Finance given to customer • Finally Collection Department collects the installments paid by customer (In case of default on finance collection department take legal action against customer)

Conclusion There are many organizations in the world which are providing consumer credit services which are helpful for the financial stability. Financial stability is very important not only for the businesses but also for the consumers. The businesses and as well as the consumers need the stability regarding the financial matters because without the stability no one could be very innovative in the longer run.

Special thanks to • Bajaj Finance – Manish Parekh

Sources of Information - Bajaj Finance - FICCI Report - Internet

Related Documents 3h463d

Presentation On Consumer Finance 3y6c2w

November 2019 27

Consumer Finance v3gw

November 2019 16

Business Model - Consumer Finance 2wu

February 2022 0

Presentation Roper Consumer Styles 2z6d2u

October 2021 0

Finance Presentation - Sample Ppt 4m494z

December 2019 34

Consumer Finance At Bank Alfalah.ppt 1848d

March 2021 0More Documents from "Bhupendra Singh Verma" 53a6q

Presentation On Consumer Finance 3y6c2w

November 2019 27

Solution Manager Expert - A Guide To Using Ca Wily Introscope For Sap Netweaver Applications 346x4s

November 2019 61

Raw Material For Smart Card Manufacturing 4v411j

December 2019 50

High Barrier Solutions For Plastic Containers Using Fluorination Process 6o4g5y

December 2019 37

Testing Of Rigid Plastic Containers 244l3g

November 2021 0